Corporate reorganization involves restructuring the way a company works in an attempt to avoid double taxation scenarios, improve profitability, or increase the company’s efficiency. The corporate reorganization clause is a provision contained in a company’s charter. The endowment directs mergers and acquisitions, changes in assets or ownership structure, as well as changes in corporate control. The most common forms of corporate reorganization include mergers and amalgamations, financial restructuring, corporate buyouts, divestitures, etc. While many companies reorganize to improve efficiency and increase profits, others also pursue reorganization as a way of reviving a financially troubled business. The management of a company facing liquidation may make certain changes to its operations.

It is the corporate action in which a company buys most, if not all, of another company ownership stakes in order to assume control. Acquisition are frequently made as part of an enterprise’s growth strategy wherever it is more valuable to take over an existing firm’s operations and niche compared to expanding on its own. A merger is alike to an acquisition but mentions more severely to combining all of the interest of both companies into a stronger single company.

The changes may include entering into an agreement with creditors on debt repayments and restructuring the company’s capital structure or the assets and liabilities. The measures are part of the company’s reorganization geared towards extending the life of the financially — troubled company.

Objectives of Merger and Acquisition

- Economies of scale

- Reduction in production, administrative, selling, legal and professional expenses

- Optimum use of capacities and factors of productions

- Tax advantages (Carry forward and set off of losses)

- Removing financial constraints for expansion

- Diversification and competitive advantage

- Revival of a week or sick company

Business Acquisition is the procedure of acquiring a company to build on strengths or weaknesses of the acquiring establishment.

Types of Business Reorganization:

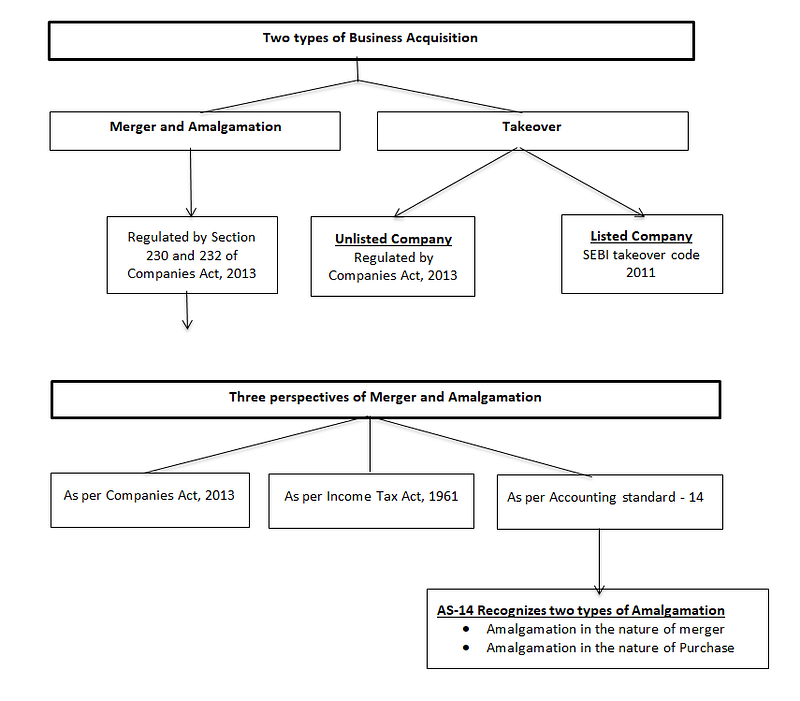

Amalgamation in the nature of merger

It affects a mode by which one company acquires another company’s assets and liabilities in such a way that, the equity shareholders of the combining entities continue to have a proportional share in the equity of the joint entity.

Amalgamation in the nature of purchase

It affects a mode by which one company acquires another company and hence, the equity shareholders of the combining entities do not continue to have an impartial share business of the acquired company is not intended to be continued after amalgamation.

Regulatory Framework of Merger & Amalgamation covers

- The Companies Act, 2013

- Companies (Compromises, Amalgamations, and agreements) Rules, 2016

- Income Tax Act, 1961

- Listing Regulations 2015

- The Indian Stamp Act, 1899

- Competition Act, 1899

- FEMA

- Banking Regulations Act, 1949

- AS-14 Companies (Indian Accounting Standard) Rules, 2015

Difference between Amalgamation and Merger

MergerAmalgamationTwo or more companies who share parallel processes or are involved in the same line of business association to expand their services or diversify their activitiesA bigger and financially stronger entity takes over a smaller one

Horizontal, vertical, and conglomeration

Amalgamation is of two types:

· the nature of purchase and

· amalgamation in the nature of merger

Merger gives rise to a new entityThe acquiring company retains its identity while the acquired company’s identity is dissolvedThe shareholders of the companies who are parties to the merger become the shareholders of the new entityShareholders of the acquired company is added to the existing number of shareholders of the acquiring company

Legal Aspects of Merger and Acquisition

Application for making compromise and arrangement

Where a compromise or arrangement is proposed –

- Among a company and its creditors or any class of them; or

- Among company and its members or any class of them.

The tribunal may, on the application of the company or of any creditors or members of the company’s or in the case of a company which is being wound up, appoint the liquidator under this Act or may be under the insolvency and Bankruptcy Code, 2016, order a meeting of the creditors or class of creditors, or of the members or class of members, to be called, held and conducted in such manner as the Tribunal directs.

Submission of additional document to the Tribunal

The company or any other person, by whom an application is made shall disclose to the Tribunal by affidavit –

- All substantial facts connecting to the company, such as the latest financial records of the company, the latest auditor’s report on the accounts of the company and the pendency of any investigation or proceedings against the company;

- Reduction of share capital of the company, included in the compromise or arrangement;

- Some arrangement of corporate debt restructuring concurred to by not less than seventy-five percent of the secured creditors in value, including

- A creditor’s responsibility statement in the prescribed from;

- Safeguarding for the protection of other secured and unsecured creditors;

- Auditor shall deliver a report that the fund requirements of the enterprise after the corporate debt restructuring as approved shall follow to the liquidity test based upon the estimates provided to them by the Board;

- Where an enterprises suggests to implement the corporate debt restructuring guidelines specified by the Reserve Bank of India, a statement to that effect; and

- A assessment report in respect of the shares and the property and all assets, tangible and intangible, movable and immovable, of the company by a registered valuer.

Some other points need to be consider

- Notice for compromise and arrangement shall be sent to all the creditors or class of creditors and to all the members or class of members and the debenture-holders of the company;

- Voting in General Meeting for objection to compromise or arrangement shall be made only by persons holding not less than ten percent of the shareholding or having outstanding debt amount which is not less than five percent of the total outstanding debt as per the newest audited financial statement.;

- Various authorities to who notice shall be sent along with all the documents to the Central Government, the income-tax authorities, the Reserve Bank of India, the securities and Exchange Board, the respective stock exchange, the official liquidator and to the Competition Commission of India; and

- Special Resolution must be passed by the appropriate persons called in the General Meeting.

Power of the Tribunal

An order made by the Tribunal shall provide for all or any of the followings matters, namely:

- When the compromise or arrangement brings for conversion of preference shares into equity shares, such preference shareholder shall be given an option to either accomplish arrears of dividend in cash or to receive equity shares equal to the value of the dividend payable;

- The protection of any class of creditors;

- Effects in the difference of the shareholders’ privileges under the compromise or arrangement;

- If creditors settled the compromises, any proceedings pendant before the Boards for Industrial and Financial Reconstruction established, of the sick Industrial Companies Act, 1987 shall abate; and

- Such other matters including departure offers to dissenting shareholders, if available, as are in the view of the Tribunal essential to effectively implement the terms of the compromise or the arrangement.

Further, tribunal shall not approved any compromise and arrangement unless a certificate by the company’s auditor has been filed with the tribunal to the effect that the accounting treatment, if any, proposed in the scheme of compromise and arrangement is in conformism with the accounting standards prescribed under section 133.

We assist our clients with all the compliances related to corporate reorganization, winding up of the company, company incorporation, business setup, ROC filings etc. If you have any questions or want to know more about corporate reorganization, kindly contact us.

Source: Corporate Reorganization